Canada Child Benefit (CCB) Calculator

Calculate your combined federal CCB and provincial child benefits for the 2026/2027 benefit year, based on your family income, province, and number of children.

tl;dr

Canadian families receive the federal Canada Child Benefit plus a provincial or territorial child benefit — all tax-free, and all income-tested on adjusted family net income (AFNI). There is no flat amount: what you get depends on how many children you have, their ages, your province, and your family net income from last year's return. This calculator estimates your combined federal and provincial total, and shows how an RRSP or FHSA contribution can raise it by lowering your AFNI.

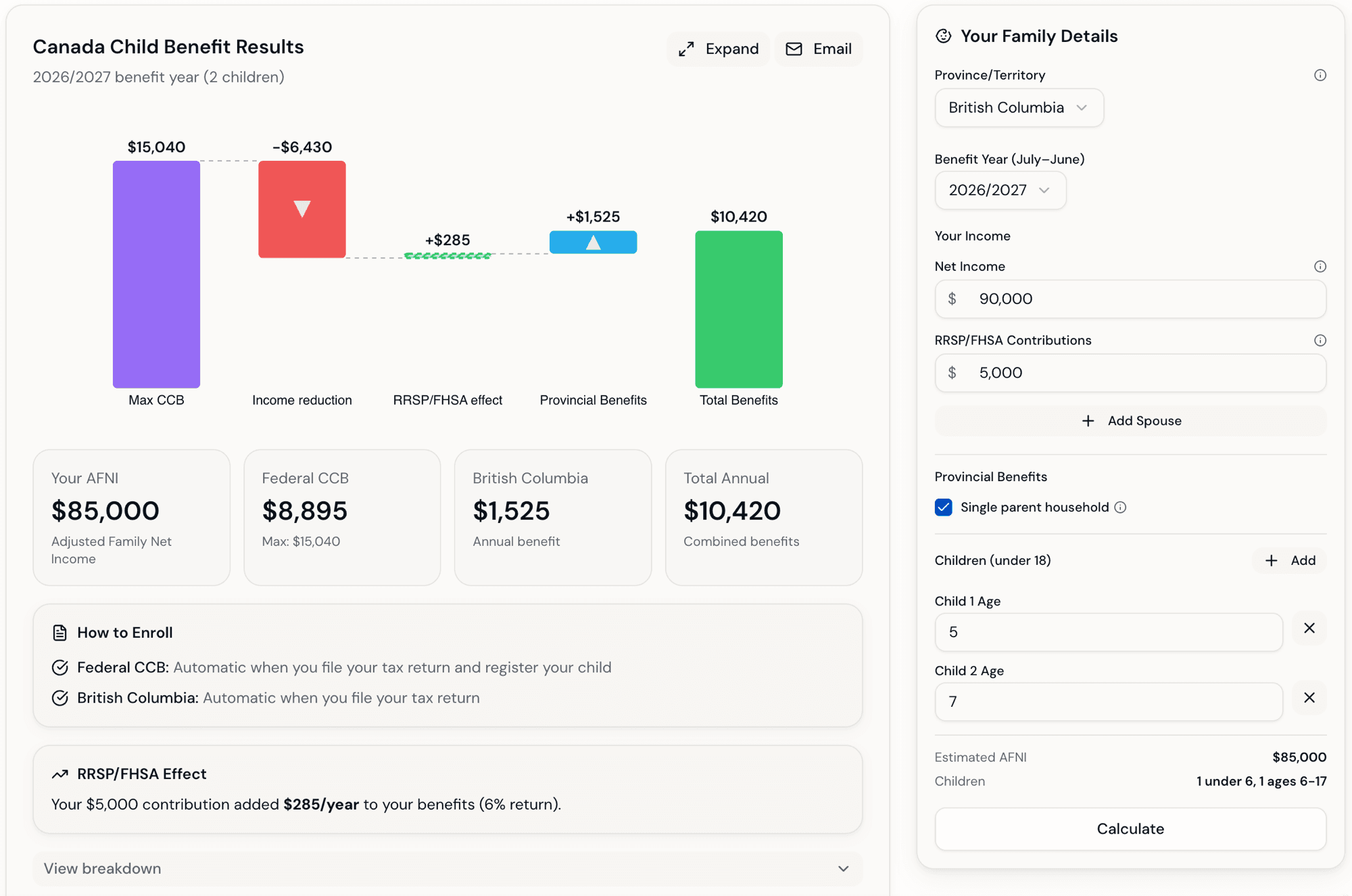

Canada Child Benefit Calculator

Estimate your combined federal CCB and provincial child benefits based on your family income and children's ages.

Both federal and provincial benefits are based on your Adjusted Family Net Income (AFNI) and reduce as income increases.

Your Family Details

Your Income

Children (under 18)

Add children to calculate CCB

Add at least one child to calculate CCB

You might also be interested in...

Related calculators that complement your financial planning

TFSA vs RRSP Calculator

Tax-Efficient Investment Strategy

Free TFSA vs RRSP calculator. Compare after-tax returns with refund reinvestment for Canadian savers. Find which account maximizes your retirement savings.

RESP Contribution Visualizer

Explore CESG & Provincial Grants

Visualize RESP grants and contribution strategies. Explore CESG, BCTESG, and QESI benefits with year-by-year projections for Canadian families.

Visual Canadian Tax Calculator

Visual Personal Tax Calculator

Free 2026 Canadian tax calculator. Calculate income tax by province with interactive Sankey diagrams, deductions, and credits.

Why CCB Calculation Matters

The Canada Child Benefit is the largest federal support program for families with children, and it's entirely tax-free. Because it's income-tested, it falls as adjusted family net income rises — and many families don't realize how sensitive it is to income changes. That creates real planning opportunities: contributing to an RRSP or FHSA to lower net income, timing bonuses or investment sales, and understanding how spousal income affects the benefit. CCB is based on the previous year's tax return, so there's a lag between an income change and the benefit change. CCB can also affect eligibility for other programs, making it a key calculation for family finances.

How Canada Child Benefit Is Calculated

CCB involves base amounts, income thresholds, and phase-out rates:

- 1. Base Amounts: There's a maximum annual benefit per child, higher for children under 6, indexed to inflation each year. The calculator uses the current amounts.

- 2. Adjusted Family Net Income: CCB is based on AFNI from your tax return (line 23600). For couples this combines both spouses' income and includes most income sources, including the taxable portion of capital gains.

- 3. First Phase-Out: Above a first income threshold, the benefit reduces at a rate that increases with the number of children.

- 4. Second Phase-Out: Above a higher threshold, a second rate applies, reducing the benefit further until it reaches zero.

- 5. Lowering AFNI: RRSP and FHSA contributions reduce AFNI, which can increase your benefit.

- 6. Monthly Payment: The annual amount is paid monthly (July to June), based on your previous year's tax return.

Boost Your CCB with RRSP and FHSA Contributions

RRSP and FHSA contributions are powerful tools for increasing your Canada Child Benefit. Both types of contributions reduce your Adjusted Family Net Income (AFNI), which is the key factor in determining your CCB amount.

RRSP Contributions

Every dollar contributed to your RRSP reduces your net income. For families in the CCB phase-out range, an RRSP contribution can meaningfully increase CCB — more so the more children you have — plus the tax refund. Try it in the calculator above.

FHSA Contributions

First Home Savings Account contributions also reduce AFNI. If you're saving for a home AND have children, FHSA contributions give you a triple benefit: tax deduction, tax-free growth, AND increased CCB.

Child Benefit Programs This Calculator Covers

On top of the federal Canada Child Benefit, every province and territory runs its own child benefit program. The calculator estimates them together, using each program's current rates:

- BC — BC Family Benefit

- AB — Alberta Child and Family Benefit (ACFB)

- SK — Saskatchewan Low-Income Tax Credit (child component)

- MB — Manitoba Child Benefit

- ON — Ontario Child Benefit (OCB)

- NB — New Brunswick Child Tax Benefit + Working Income Supplement

- NS — Nova Scotia Child Benefit

- PE — PEI Child Benefit

- NL — Newfoundland and Labrador Child Benefit

- YT — Yukon Child Benefit

- NT — Northwest Territories Child Benefit

- NU — Nunavut Child Benefit + Territorial Workers' Supplement

Quebec's Family Allowance is administered separately by Retraite Québec and isn't included in the combined estimate.

2026/2027 CCB Payment Schedule

All 12 payments in the 2026/2027 benefit year (July 2026 – June 2027) are based on your 2025 tax return. Your benefit amount is recalculated every July from your newest return.

Jul – Dec 2026

benefit year

Same benefit year — all payments based on your 2025 return

Jan – Jun 2027

Plan ahead for the next recalculation: Your CCB is recalculated in July 2027 from your 2026 tax return. An RRSP contribution before the March 1, 2027 deadline reduces your 2026 net income, increasing your CCB for the entire 2027/2028 benefit year (Jul 2027 – Jun 2028).

Common Questions

How much CCB will I get?

There is no flat amount. The Canada Child Benefit is income-tested, so your payment depends on the number of children you have, their ages, your province or territory, and your adjusted family net income (AFNI) from last year's tax return. Families under the first income threshold receive the maximum for each child; above it the benefit phases out at a rate that rises with the number of children. Because most provinces add their own child benefit on top, two families with identical incomes in different provinces can receive noticeably different totals. Enter your details above for an estimate of your combined federal and provincial amount.

Is the child tax benefit the same as the Canada Child Benefit?

Effectively, yes. "Child tax benefit" is what most people still call it, from the old Canada Child Tax Benefit (CCTB) and the Universal Child Care Benefit (UCCB). Both were replaced in 2016 by the Canada Child Benefit, which rolled them into a single tax-free monthly payment that is income-tested rather than universal. If you are searching for a child tax benefit calculator, this is the right tool — the CCB is the current program.

When do I need to apply for CCB?

Apply as soon as your child is born or begins living with you — online through CRA My Account, by mail, or automatically when registering a birth in some provinces. Payments can be retroactive, but applying early avoids missed payments.

What provincial child benefits are available?

Every province and territory adds its own child benefit on top of the federal CCB — for example the Ontario Child Benefit, BC Family Benefit, Alberta Child and Family Benefit, and Quebec's Family Allowance (administered separately). Most phase out as family income rises.

Do I need to apply separately for provincial benefits?

In most provinces you're automatically enrolled when you file your tax return and receive federal CCB. Manitoba requires a separate provincial application, Quebec administers its own family benefits through Retraite Québec, and Saskatchewan's Employment Incentive requires a separate application.

Does CCB count as income or affect my taxes?

No — both federal CCB and provincial child benefits are tax-free and don't need to be reported as income. However, eligibility is based on your Adjusted Family Net Income, so your tax situation affects how much you receive.

Can I increase my benefits by contributing to my RRSP or FHSA?

Yes — both RRSP and FHSA contributions reduce your Adjusted Family Net Income, which can increase federal CCB and provincial benefits. This is most valuable for families near a phase-out threshold. The calculator shows the effect.

What if I'm separated or share custody?

For shared custody, CCB can be split between the two parents, each receiving a portion of the benefit. The primary caregiver typically receives CCB in non-shared situations. Provincial benefits follow similar rules.

Do I need to reapply every year?

No — as long as you file your tax return every year, the CRA automatically recalculates your CCB from your updated income. Most provincial benefits are recalculated automatically too. Your July payment reflects your most recently filed return.

What are the CCB income thresholds?

CCB begins reducing once family net income passes a first threshold, with a reduction rate that rises with the number of children, and a second phase-out at a higher threshold. The calculator uses the current thresholds; provincial benefits have their own.

Maximizing Your Canada Child Benefit

- ✓File Taxes on Time: CCB is recalculated each July from your return. File on time to keep payments uninterrupted.

- ✓Maximize RRSP Contributions: RRSP contributions reduce your net income, which can increase your CCB — most impactful near a phase-out threshold.

- ✓Time Capital Gains: Since the taxable portion of a gain raises your net income, time large sales to limit the impact on CCB.

- ✓Claim All Deductions: Childcare, moving, and other deductions reduce net income and can increase CCB. Don't miss eligible deductions.

- ✓Keep CRA Updated: Report changes in custody, marital status, or address promptly. Incorrect payments must be repaid.

- ✓Budget Annually: CCB is recalculated every July, so an income increase lowers payments starting in July. Budget for it.

- ✓Apply for Provincial Benefits: Most provinces add child benefits, and CCB often determines eligibility automatically.